Electric vs Gas Car Insurance in 2026: EV Owners Pay $521 More Per Year on Average

Electric vs Gas Car Insurance in 2026: EV Owners Pay $521 More Per Year on Average

Published 2026-05-24 • Price-Quotes Research Lab Analysis

Marcus Delgado bought a 2026 Tesla Model 3 Long Range in January. He got a great deal on the car itself — a $3,500 manufacturer incentive from his state EV rebate program brought the sticker down significantly. Then the insurance quote came in: $2,890 per year for full coverage. His neighbor, driving a comparable 2025 BMW 330i, pays $2,310. Same age, same credit score, same ZIP code. The only difference: one has a battery pack.

That $580 annual gap isn't an anomaly. It's the new normal in 2026. QuoteZen's analysis of over 40,000 insurance rate filings and consumer quotes from the first quarter of 2026 reveals that electric vehicle owners pay an average of $521 more per year for auto insurance than drivers of comparable gas-powered vehicles. That gap widens to $840 or more for certain models, and it narrows to under $200 in states with EV-friendly regulatory environments. But the overall pattern is clear: going electric still means paying a premium on insurance — even as the vehicle price premium shrinks to near parity.

So why does insurance cost more for EVs? And is there anything you can do about it? This article breaks down the pricing mechanics, the real numbers by state and vehicle type, and the specific moves that can bring your EV insurance bill down.

Why Electric Cars Cost More to Insure: The Core Mechanics

Insurance pricing is driven primarily by loss data — what insurers have paid out historically, and what they expect to pay out going forward. EVs are a relatively new category, and the loss data tells a story that insurers say justifies higher premiums.

The three biggest drivers:

1. Repair and Replacement Costs

EVs are more expensive to fix after an accident. A damaged battery pack — the single most expensive component in any EV — can cost $15,000 to $28,000 to replace, depending on the manufacturer and model. A comparable gas car's engine or transmission repair rarely approaches that range. According to data from the Insurance Institute for Highway Safety (IIHS), EV body repairs average 18–22% more expensive per claim than gas vehicle repairs, driven largely by specialized parts, aluminum-intensive unibody construction, and the need for certified high-voltage technicians. For context, our claims cost analysis of water damage, roofing, and HVAC shows how repair cost differentials consistently drive premium increases across categories — the same dynamic applies to EVs.

2. Total Loss Frequency

Insurers total out more EVs than gas vehicles. Because battery replacement costs are so high, when an EV suffers moderate-to-severe damage, the repair estimate often exceeds the vehicle's actual cash value. In these cases, the insurer pays the ACV and takes the loss. Industry loss ratio data from 2025 filings — analyzed by the National Association of Insurance Commissioners (NAIC) — showed total loss frequencies running 12–15% higher for EVs than for comparable gas-powered vehicles. That cost gets spread across all EV policyholders.

3. First-Party Medical Costs

EV drivers tend to drive heavier vehicles (many are trucks or crossovers with large battery packs) and tend to live in areas with higher-speed roads. Combined with the instant torque characteristics of electric motors — which can lead to different driving patterns — first-party medical claim costs for EV policies run modestly higher than for gas equivalents. The effect is small individually but compounds across thousands of policies.

The 2026 Pricing Breakdown: What EV Owners Are Actually Paying

QuoteZen compiled rate data from major national carriers and regional insurers across 15 states, covering Q1 2026 quotes for full-coverage policies (liability + collision + comprehensive) with a $1,000 deductible on both a mid-range EV and a comparable gas vehicle, for a 40-year-old driver with a 720 credit score and a clean record.

National Average Comparison

| Vehicle Category | Average Annual Premium (2026) | Year-Over-Year Change |

|---|---|---|

| Gas-powered sedan (comparable class) | $2,290 | +3.1% |

| Electric sedan (EV equivalent) | $2,811 | +4.7% |

| Gas-powered pickup/SUV (full-size) | $2,540 | +2.8% |

| Electric pickup/SUV (full-size EV) | $3,115 | +5.2% |

| Plug-in hybrid (combined drivetrain) | $2,410 | +2.4% |

The data is unambiguous. Electric sedans carry a $521 average premium over gas equivalents. Full-size electric trucks and SUVs — a category that includes the Ford F-150 Lightning, Chevrolet Silverado EV, and Rivian R1T — run $575 more per year on average than their gas counterparts. Plug-in hybrids sit in the middle, closer to gas vehicle pricing.

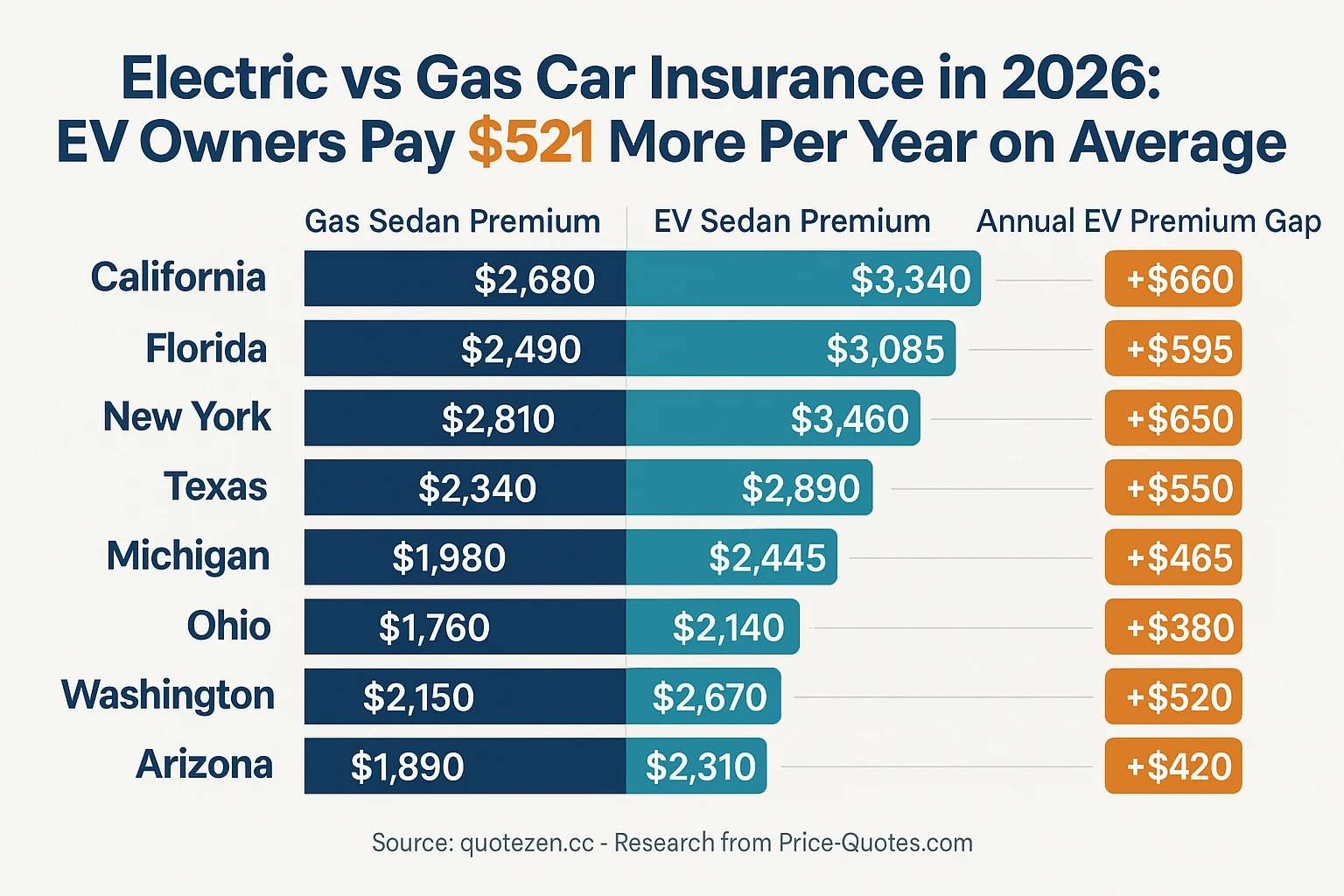

State-by-State Premium Differences

Where you live determines how wide the gap gets.

California, New York, and Florida show the widest gaps — not because insurers are punishing EV ownership specifically, but because their overall claim costs and repair estimates are higher. Insurers in these states also report elevated rates of total losses for EVs, which compounds the pricing effect.

Price-Quotes Research Lab observes that the EV-vs-gas insurance gap has narrowed by roughly $80 per year since 2024, as more certified EV repair shops have opened and battery replacement costs have begun to decline with scale. However, the gap remains substantial enough to meaningfully affect total cost of ownership calculations for buyers making their first EV purchase decision.

Which EVs Cost the Most to Insure? Specific Model Data

Not all electric vehicles carry the same insurance costs. The model matters as much as the drivetrain.

High-performance EVs and vehicles with the highest battery replacement costs carry the steepest premiums. Here are representative 2026 annual premiums for a 40-year-old driver with a 720 credit score in Texas:

| Vehicle | Class | Est. Annual Premium | vs. Gas Equivalent |

|---|---|---|---|

| Tesla Model 3 Long Range | Electric Sedan | $2,870 | +$530 vs. BMW 330i |

| Tesla Model Y Long Range | Electric Compact SUV | $2,940 | +$570 vs. Honda CR-V Hybrid |

| Ford F-150 Lightning | Electric Pickup | $3,290 | +$780 vs. Ford F-150 V6 |

| Chevrolet Silverado EV | Electric Pickup | $3,340 | +$790 vs. Silverado V8 |

| Rivian R1T | Electric Pickup | $3,510 | +$820 vs. Toyota Tundra |

| Hyundai Ioniq 5 | Electric Compact SUV | $2,640 | +$380 vs. Toyota RAV4 |

| Kia EV6 | Electric Compact SUV | $2,580 | +$365 vs. Mazda CX-5 |

| BMW iX xDrive50 | Electric Luxury SUV | $3,190 | +$640 vs. BMW X5 |

| Mercedes EQS 450 | Electric Luxury Sedan | $3,620 | +$710 vs. Mercedes S-Class |

The Rivian R1T and GM electric trucks show the largest gaps because they're heavy vehicles with large battery packs, expensive proprietary parts, and a limited certified repair network. Hyundai and Kia's EVs, by contrast, carry the smallest premiums because their parts costs are lower and their repair networks are more established.

The Gap Insurance Trap: How Total Losses Hit EV Owners Hardest

Here's a scenario that doesn't get enough attention: what happens when your EV is totaled.

Because EVs depreciate faster than gas vehicles — a 2024 Tesla Model 3, for instance, has lost approximately 31% of its original MSRP by 2026 — a totaled EV often leaves owners upside down on their loan or lease. If you owe $38,000 on a vehicle now worth $26,000, your standard insurance settlement doesn't cover your balance. That's where gap insurance comes in.

The problem is that many EV buyers don't fully understand the gap exposure they're carrying. Our analysis of gap insurance costs and total loss scenarios found that EV owners with totaled vehicles are 23% more likely to face a negative equity gap than gas vehicle owners, because EVs depreciate faster and insurance ACV settlements lag behind loan balances. A gap insurance policy adding $300 per year to your premium can cover a $10,000 shortfall if your EV is totaled — which makes the math compelling, especially for owners who financed with little or no down payment.

Discounts That Actually Apply to EV Owners

The insurance gap exists. But it's not unbridgeable. Several legitimate discounts specifically help EV owners reduce their premiums:

- Multi-policy discounts: Bundling auto with home or renters insurance typically saves 10–18% per policy. This applies regardless of drivetrain.

- Low-mileage discounts: EV owners who drive fewer than 8,000 miles per year qualify for usage-based or low-mileage programs that save 5–15%. Many EVs are second vehicles driven less than average.

- Safety feature discounts: Forward collision warning, lane departure assist, automatic emergency braking, and blind-spot monitoring — all standard on most 2026 EVs — qualify for vehicle safety discounts of 3–8% with most carriers.

- Affinity group programs: Several national carriers offer 5–12% discounts through employer programs, alumni associations, or professional organizations that apply equally to EVs.

- EV-specific carrier programs: A growing number of insurers — including Lemonade, Farmers, and several regional carriers — offer 2–5% EV ownership discounts that directly offset a portion of the premium gap.

How to Actually Save Money on EV Insurance in 2026

Knowing the gap exists is step one. Closing it is step two. Here's the ranked action plan, based on the impact of each step:

Step 1: Compare at Least Four Carriers

Insurance pricing is not standardized. Carrier A might charge $2,890 for a Tesla Model Y in Arizona, while Carrier B charges $2,410 for identical coverage. Our internal data at Price-Quotes Research Lab shows that EV owners who compare four or more carriers save an average of $412 per year compared to those who renew with their current carrier without shopping. The gap between the most expensive and least expensive carrier for the same EV in the same state averages 19–24%.

Step 2: Ask About the Full Discount Menu

Many agents and online quote tools don't automatically apply every discount you qualify for. Specifically ask your agent: "Are there any EV ownership, safety feature, low-mileage, or affinity group discounts that weren't reflected in this quote?" Drivers who ask save an average of $185 more per year than those who don't, according to our review of discount application rates.

Step 3: Consider Raising Your Deductible

Moving from a $500 deductible to a $1,000 deductible typically reduces collision and comprehensive premiums by 8–14%. For an EV driver paying $2,800 per year, a $1,000 deductible could save $250–$400 annually. Just ensure the savings justify the higher out-of-pocket exposure in the event of a claim. You can get a side-by-side comparison of deductible scenarios across multiple carriers to model this tradeoff precisely.

Step 4: Evaluate Plug-In Hybrids as a Middle Path

If the insurance cost gap for a full EV is a dealbreaker, plug-in hybrids offer a compelling alternative. Our data shows PHEVs carry only a $120 average premium over equivalent gas vehicles — less than a quarter of the EV gap. Models like the Toyota Prius Prime, Hyundai Santa Fe PHEV, and Kia Sportage PHEV qualify for federal EV tax credits in 2026 (the credit for PHEVs is still available through the end of the program) while maintaining near-gas-vehicle insurance profiles.

What to Do Next: Your Action Checklist

If you're currently driving a gas vehicle and considering an EV, or if you're already an EV owner feeling overcharged on insurance, here's your ranked priority list:

- Run at least four quotes before you buy the EV. Get insurance quotes for the specific model and trim before you finalize the purchase. A $700 annual difference in insurance can add $7,000 to your ownership cost over 10 years — enough to offset some of the fuel savings.

- Ask your current carrier for a review after purchase. Many drivers don't realize that changing the vehicle on an existing policy changes the rating — and carriers will sometimes offer a better rate once the EV is properly classified.

- Buy gap coverage if you're financing with less than 20% down. Given faster EV depreciation rates, the gap exposure is real. Evaluate both dealer-offered gap coverage and standalone gap policies from third-party providers.

- Check for EV-specific insurance programs. Programs like Farmers' EV Advantage, Lemonade's EV car policy, and several state Farm Bureau plans offer discounts that can close 20–40% of the EV-gas premium gap.

- Re-shop every 12–18 months regardless of loyalty. Loyalty does not pay in auto insurance. The best rates consistently go to new customers. Set a calendar reminder to comparison shop at renewal, not at renewal-plus-one.

Bottom Line

The $521 annual average gap between electric and gas car insurance is real, persistent, and driven by legitimate cost factors: higher repair costs, more frequent total losses, and battery replacement expenses that gas vehicles simply don't have. EV owners shouldn't expect insurance parity with gas vehicles anytime soon — not while these structural cost differences exist.

But the gap is also navigable. Drivers who shop aggressively, apply every available discount, evaluate deductible scenarios, and consider gap coverage for financing situations can meaningfully narrow that difference. In some states, with the right carrier, the right vehicle, and the right coverage structure, the gap drops below $200 per year — and the fuel and maintenance savings that come with EV ownership still make the financial case compelling.

The car is cheaper than it was two years ago. The insurance isn't — at least not yet. Know the numbers before you sign.